완료

2020 FRM Part1 Financial Market & Product 박정준 강사님

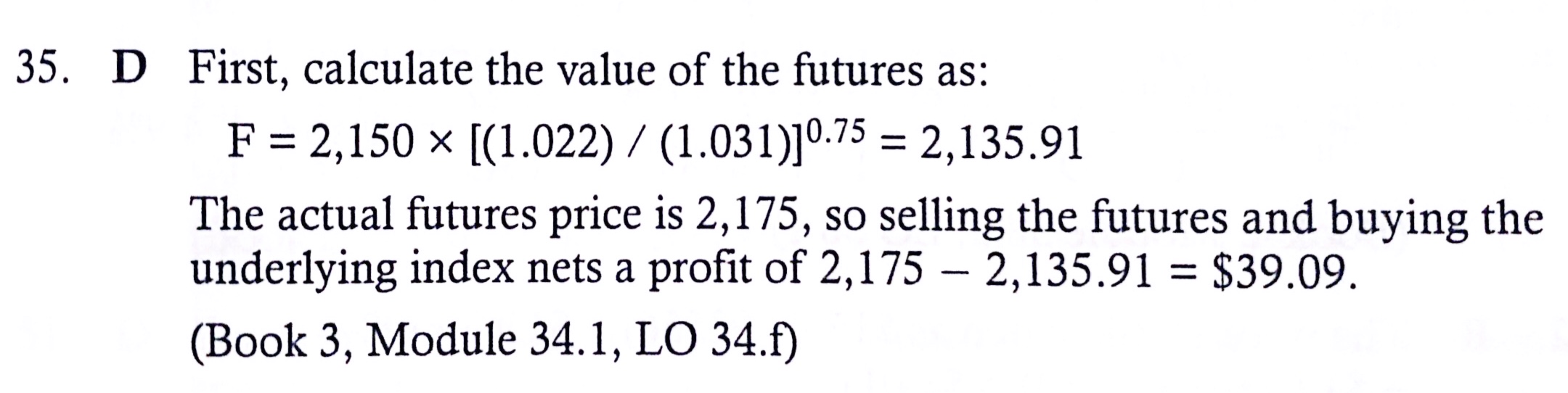

- 2020 practice exam 12p 35번 9-month future 문제에서

- underlying asset (index)= 2150 dividend=2.2%, risk-free risk=3.20%라고

- 되어 있어서 선물가격은 F = 2150*(1.031/1.022)^(9/12) 구하는게 틀린건가요??

- (35p 풀이과정에는F = 2150*(1.022/1.031)^(9/12)적혀 있어서 제가 잘 못하는건지 궁금합니다)

- 또 답을 보면 차익거래 이익을 $로 표현했는데 그러면 index이므로 $250(S&P500기준) 을 고려해서 해야하는거 아닌가요?

- 답지에는 가치 차이만 고려해서 거기다가 그냥 $를 붙혔는데 헷갈립니다.

- A 9-month futures contract on the S&P 500 is currently priced at 2,175. The underlying stocks within the index are valued at 2,150 and pay dividends at an annual rate of 2.20%. The risk-free rate is currently 3.10%. Assuming a trader wants to attempt to profit through a potential arbitrage opportunity, which of the following statements is correct?

A. The trader should buy the futures and sell the stocks in the index for an arbitrage profit of $25.

B. The trader should buy the stocks in the index and sell the futures contract for an arbitrage profit of $25.

C. The trader should buy the futures and sell the stocks in the index for an arbitrage profit of $39.

D. The trader should buy the stocks in the index and sell the futures contract for an arbitrage profit of $39.

0

댓글

안녕하세요? 박정준입니다.

선물의 이론가격(FP)은 현물가격 + Carrying Cost ? Carrying Benefit 입니다.

문제에서 금리(r)는 대표적인 Cost이고, 배당은 대표적인 Benefit이니,

FP = S * [(1 + 금리) / (1 + 배당률)]^(만기)로 계산하는 것이 맞습니다.

단위와 관련하여는

문의주신 대로 차익거래 이익에 $ 표기를 하는 것은 적절하지 않아 보입니다. 39.09pt 만큼 선물이 고평가되어 있다고 판단해야 합니다.

감사합니다.

댓글을 남기려면 로그인하세요.