CFA L3_Currency Management_Curriculum Book_김종곤 강사님

안녕하세요 강사님,

항상 어려운 과목들을 원리부터 쉽게 설명해주셔서 지금까지 너무 감사히 배워올 수 있었습니다. 감사합니다!

커리큘럼북 45번 문제의 답이 맞는 걸까요? 이래저래 풀어봐도 이해가 안돼서 Chat GPT에게 물어보니 저랑 같은 방식으로 풀어주더라구요^^;; 강사님의 명쾌한 설명 부탁드립니다~! 항상 감사드립니다!

Derivatives and Risk Management : Currency Management: An Introduction

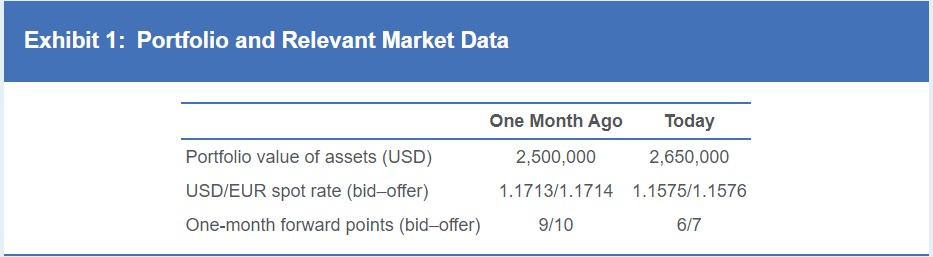

45. Rivera’s reporting currency is the euro, and he is concerned about his US dollar exposure. His portfolio IPS requires monthly rebalancing, at a minimum. The portfolio’s market value is USD2.5 million. Given Rivera’s risk aversion, Delgado is considering a monthly hedge using either a one-month forward contract or one-month futures contract.

Calculate the net cash flow (in euros) as of today to maintain the desired hedge. Show your calculation.s.

Solution

When hedging one month ago, Delgado would have sold USD2,500,000 one month forward against the euro.

To calculate the net cash flow (in euros) today, the following steps are necessary:

- Sell USD2,500,000 at the one-month forward rate stated in the forward contract. Selling US dollars against the euro means buying euros, which is the base currency in the USD/EUR forward rate. Therefore, the offer side of the market must be used to calculate the inflow in euros.

All-in forward rate = 0.8914 + (30/10,000) = 0.8944

USD2,500,000 / 0.8944 = EUR2,795,169.95. - Buy USD2,500,000 at the spot rate to offset the USD sold in Step 1 above. Buying the US dollar against the euro means selling euros, which is the base currency in the USD/EUR spot rate. Therefore, the bid side of the market must be used to calculate the inflow in euros.

USD2,500,000 / 0.8875 = EUR2,816,901.41. - Therefore, the net cash flow is equal to EUR2,795,169.95 – EUR2,816,901.41, which is equal to a net outflow of EUR21,731.46.

To maintain the desired hedge, Delgado will then enter into a new forward contract to sell the USD2,650,000. There will be no additional cash flow today arising from the new forward contract.

댓글

안녕하세요. 이패스코리아 입니다.

강사님께 문의 후 답변 전달 드리겠습니다.

감사합니다.

안녕하세요,

시험이 얼마 남지 않아서 강사님께 한번 더 문의 부탁드립니다~!

감사합니다.

안녕하세요?

답변이 늦어 죄송합니다.

일단 이 예제는 문제의 풀이가 틀렸습니다. 한달 전 USD Exposure는 $2,500,000였고 오늘 USD Exposure는 $2,650,000이니까 한달 전 $2,500,000 Exposure를 전부 헤지했다고 가정하면 Sell USD/Buy Euro One-month Forward 환율을 이 표에서 주어진 환율로 계산하면 1/1.1714 + 10/10,000 = 0.8537+ 0.0010 = 0.8547입니다. 이렇게 한달 전 실행했던 Sell USD/Buy Euro Forward를 오늘 청산하고 다시 한달 연장하려면 $2,500,000에 대해서는 Buy USD/Sell Euro 현물 환율(1/1.1575 = 0.8639)로 Position 청산이 필요하고 다시 $2,650,000에 대한 Sell USD/Buy Euro One month Forward가 필요합니다(Mismachted F/X Swap).

감사합니다.

김종곤

댓글을 남기려면 로그인하세요.